What you need to know

Under current law, more than 20 million Americans receive subsidies to purchase health insurance through state-administered insurance exchanges. The original legislation that established these subsidies is the Affordable Care Act (ACA), also known as “Obamacare”. A large chunk of these subsidies will expire on December 31, 2025, unless Congress extends them. This brief explains:

- What the subsidies are, the intent behind why they were included in the ACA, and the reasoning for why they were expanded in 2021.

- The possible consequences and impact of allowing the subsidies to expire or extend.

What are ACA Subsidies?

The ACA created insurance exchanges where individuals and families can purchase health insurance. The goal was to reduce the number of uninsured people in two groups: (a) people who have low incomes, but who make too much to qualify for Medicaid (the federal health program geared towards people with limited income and resources) and are too young to qualify for Medicare (the federal health program for Seniors and certain younger people with specific conditions), and (b) people who exceeded certain limits above the federal poverty level (FPL) but who did not have access to health insurance from their employer.

In the current ACA exchanges, insurers offer different levels of insurance. The highest-cost Gold plans offer the highest level of coverage and low deductibles; the cheaper Silver plans offer fewer benefits and higher deductibles; and the cheapest Bronze plans offer the least benefits and the highest deductibles. Individuals choose a plan, and the subsidies are paid directly to the insurer.

The ACA included subsidies to reduce the cost of insurance to many of these individuals. Initially, subsidies were available to households with incomes between 100% and 400% of the FPL, which is currently about $32,000 to $128,000 for a family of four. These subsidies were designed as a sliding-scale benefit so that lower-income households received larger subsidies than higher-income households.

Congress expanded the ACA subsidies during the COVID pandemic as part of the American Rescue Plan, enacted in 2021. Individuals and families with incomes below 150% of the FPL can receive free Silver-level coverage. Moreover, individuals and families with incomes above 400% of the FPL can receive a subsidy if a Silver-level plan would cost more than 8.5% of their income. Subsidies were also added for gig workers and early retirees. However, these expanded subsidies were set to expire on December 31, 2025.

What is the impact of the ACA subsidies?

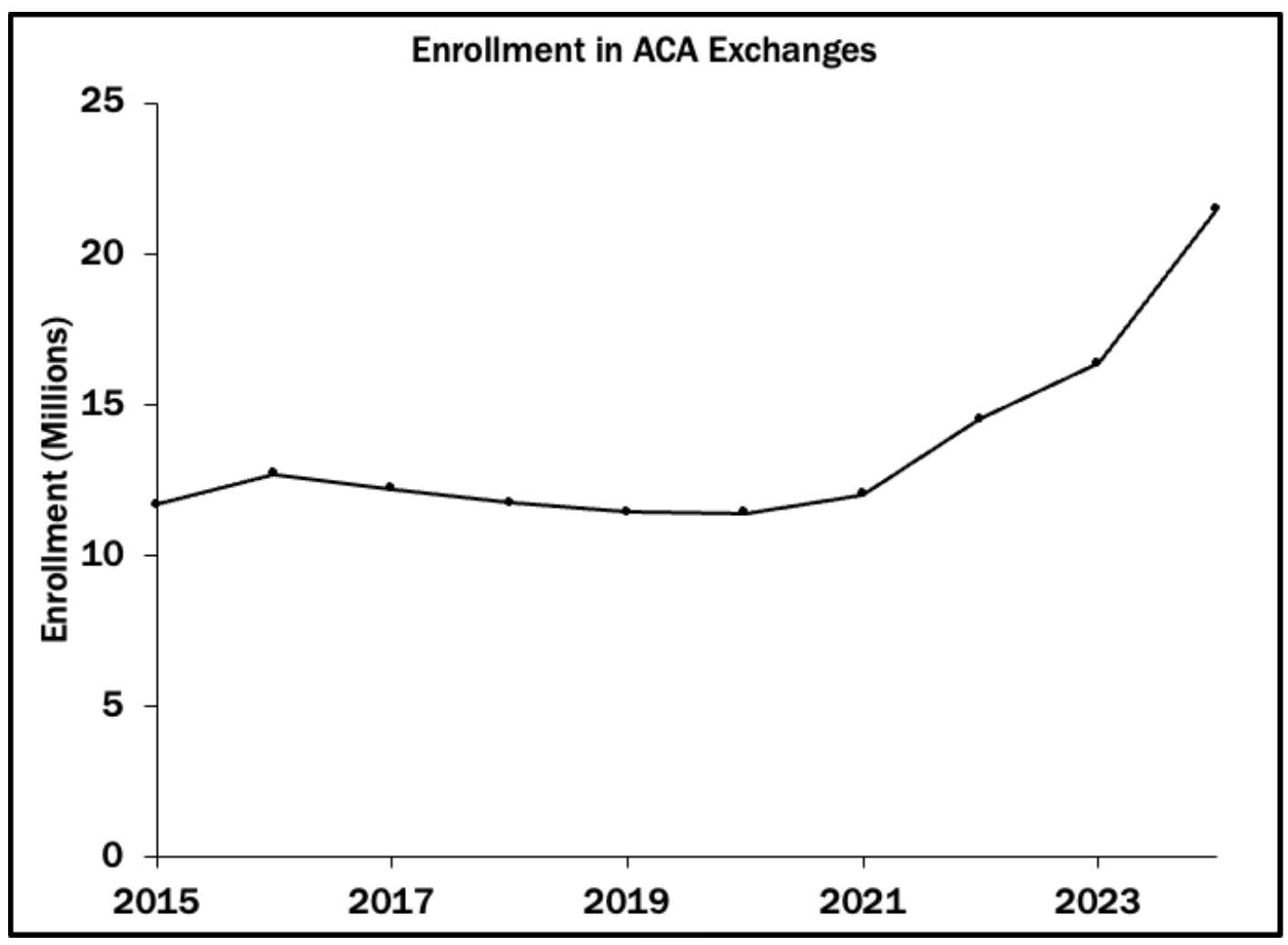

After the enhanced ACA subsidies were established in 2021, the number of individuals receiving insurance through the exchanges increased significantly (by about 10 million, or 3% of the population), as shown below.

However, data from the Kaiser Family Foundation shows that the uninsured rate in the U.S. declined only somewhat, from 9.2% in 2020 to 7.9% in 2023, suggesting that about half of the new enrollees previously had insurance from another source (such as an early retiree who received insurance from their employer prior to their retirement).

Because ACA recipients have to re-select a plan each year, insurers have already begun sending notices detailing 2026 rates that do not include subsidies. In some cases, recipients face significant premium increases, up to 50-100% above their current payments.

The actual increase recipients will pay depends on which plan they select. For example, someone facing a higher Silver plan cost might choose a Bronze plan or a lower-cost Silver plan instead. It is also the case that health insurance costs are rapidly increasing for all Americans, meaning some of the ACA premium increases are due to higher health care costs rather than reduced subsidies.

The main objections to extending the current subsidies are (a) they are estimated to cost the federal government about $1.1 trillion over the next decade, which is about 10% of total federal health care spending, (b) the subsidies were not originally designed to be permanent, and (c) the availability of subsidies means that recipients have a smaller incentive to comparison-shop for the most-effective, cheapest plan, and insurers have less of a reason to compete by offering lower prices.

The Takeaway

Health insurance subsidies created during the COVID pandemic are set to expire on December 31, 2025.

There are sharp tradeoffs faced when designing social policies. Adding the subsidies has increased the number of Americans using the exchanges by about 3%, or 10 million individuals, and reduced the uninsured rate by about 1.3%.

This increase in insurance coverage, however, comes at a cost: a healthcare system that may otherwise lack strong incentives for insurers to improve efficiencies and drive down premiums, the direct cost on tax payers absorbing the subsidies, and the forgone opportunity cost of spending these funds elsewhere, whether in health care or another area, reducing taxes, or paying down the national debt.

Enjoying this content? Support our mission through financial support.

Further reading

Harvard Kennedy School. (2025). The health insurance subsidies behind the government shutdown. https://tinyurl.com/9jrhmup4, accessed 12/09/25.

Peter G. Peterson Foundation. (2024). How Does the Federal Government Subsidize Healthcare Under the ACA - and What Does It Cost? https://tinyurl.com/2cbmjf8e, accessed 12/09/25.

Sources

Congressional Budget Office. (2025). Major Recurring Reports. https://tinyurl.com/yu2en3yk, accessed 12/09/25.

Centers for Medicare & Medicaid Services. (2025). 2025 Marketplace Open Enrollment Period Public Use Files. https://tinyurl.com/4c7xy3d4, accessed 12/09/25.

ASPE. (2013). 2013 Poverty Guidelines. https://tinyurl.com/2pvswpum, accessed 12/09/25.

IRS. (2025). Small Business Health Care Tax Credit and the SHOP Marketplace (ACA). https://tinyurl.com/47upv6ur, 12/09/25.

Congressional Budget Office. (2012). CBO Releases Updated Estimates for the Insurance Coverage Provisions of the Affordable Care Act. https://tinyurl.com/22ae8wzv, accessed 12/09/25.

ASPE. (2016). Health Plan Choice and Premiums in the 2017 Health Insurance Marketplace. https://tinyurl.com/mrymkrfa, accessed 12/09/25.

Contributors

Lindsey Cormack (Content Lead) is an Associate Professor of Political Science at Stevens Institute of Technology and the Director of the Diplomacy Lab. She received her PhD from New York University. Her research explores congressional communication, civic education, and electoral systems. Lindsey is the creator of DCInbox, a comprehensive digital archive of Congress-to-constituent e-newsletters, and the author of How to Raise a Citizen (And Why It’s Up to You to Do It) and Congress and U.S. Veterans: From the GI Bill to the VA Crisis. Her work has been featured in The New York Times, The Washington Post, Bloomberg Businessweek, Big Think, and more. With a drive for connecting academic insights to real-world challenges, she collaborates with schools, communities, and parent groups to enhance civic participation and understanding.

William Bianco (Research Director) is Professor of Political Science at Indiana University and Founding Director of the Indiana Political Analytics Workshop. He received his PhD from the University of Rochester. His teaching focuses on first-year students and the Introduction to American Government class, emphasizing quantitative literacy. He is the co-author of American Politics Today, an introductory textbook published by W. W. Norton, now in its 8th edition, and has authored a second textbook, American Politics: Strategy and Choice. His research program is on American politics, including Trust: Representatives and Constituents, and numerous articles. He was also the PI or Co-PI for seven National Science Foundation grants and a current grant from the Russell Sage Foundation on the sources of inequalities in federal COVID assistance programs. His op-eds have been published in The Washington Post, Indianapolis Star, Newsday, and other venues.