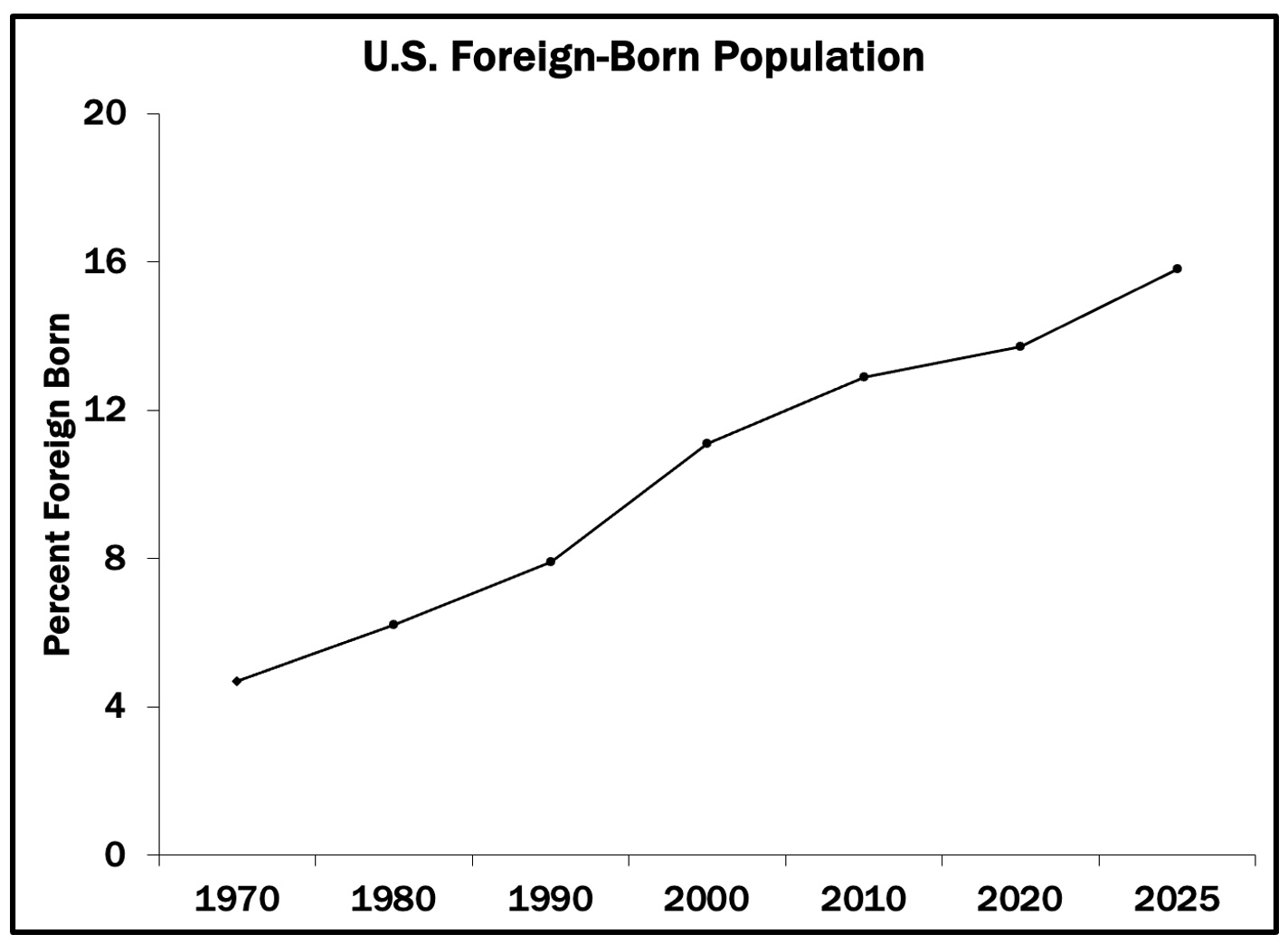

What is Federalism?

Federalism is a system in which some policy-making powers are exercised by the national government, some by state and local governments, and some are shared between different levels. America has a federal system: for example, the national government is responsible for defense, state and local governments administer elections, and both levels share responsibility for areas such as health policy.

The main advantage of federalism is that local governments often have better information about local needs and can shape policy to address these concerns. Federalism also allows communities to decide which services they want (and how much they want to pay in taxes) rather than being subject to national mandates. The disadvantage of federalism is that the level of services an individual receives from the government varies depending on where they live. For more on federalism, see our brief.

Who were the Federalists and the Antifederalists?

During the Founding, Federalists such as Alexander Hamilton and James Madison favored increasing the power of the national government, having it assume many responsibilities that state governments had exercised. As Madison wrote in Federalist 10, the goal was to “cure the mischiefs of faction” - to increase the chances that governments would address the needs of large majorities rather than small groups. Madison also argued that the proposed Constitution gave most power to the states, noting in Federalist 45, “The powers delegated by the proposed Constitution to the federal government are few and defined. Those which are to remain in the State governments are numerous and indefinite.”

The Antifederalists opposed the Federalists. Most Antifederalists favored amending the Articles of Confederation (the system of government in place during the Revolutionary War), but wanted most policymaking power to remain at the state level. They feared that a strong national government would impose policies on states and localities, preventing communities from acting as they thought best.

What did Elbridge Gerry want?

Elbridge Gerry was a prominent Antifederalist. He was a state legislator from Massachusetts and a delegate at the Constitutional Convention who later became the Governor of Massachusetts. His name is where the term “gerrymandering” (the practice of shaping legislative districts for political advantage) comes from.

Throughout the Convention, Gerry was a frequent speaker and member of committees tasked with resolving difficult issues. Initially, Gerry did not support the proposed Constitution. However, he made clear in a letter to members of the Massachusetts legislature that he would support a revised document:

My principal objections to the plan, are, that there is no adequate provision for a representation of the people — that they have no security for the right of election — that some of the powers of the legislature are ambiguous, and others indefinite and dangerous — that the executive is blended with, and will have an undue influence over, the legislature — that the judicial department will be oppressive — that treaties of the highest importance may be formed by the president with the advice of two-thirds of a quorum of the senate — and that the system is without the security of a bill of rights. These are objections which are not local, but apply equally to all the states.

The constitution proposed has few if any federal features; but is rather a system of national government. Nevertheless, in many respects, I think it has great merit, and, by proper amendments, may be adapted to the "exigencies of government, and preservation of liberty."

Ultimately, the efforts of Gerry and other Antifederalists led to an important compromise: the new Congress would adopt additional restrictions on the national government, which we now know as the first 10 amendments to the Constitution, the Bill of Rights. These amendments limited the national government’s power to regulate individual liberties, such as freedom of speech. The 10th Amendment also addressed Federalism directly: “The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are reserved to the States respectively, or to the people.” With the promise of these changes, Gerry supported ratification of the Constitution.

What would Gerry think about present-day federalism?

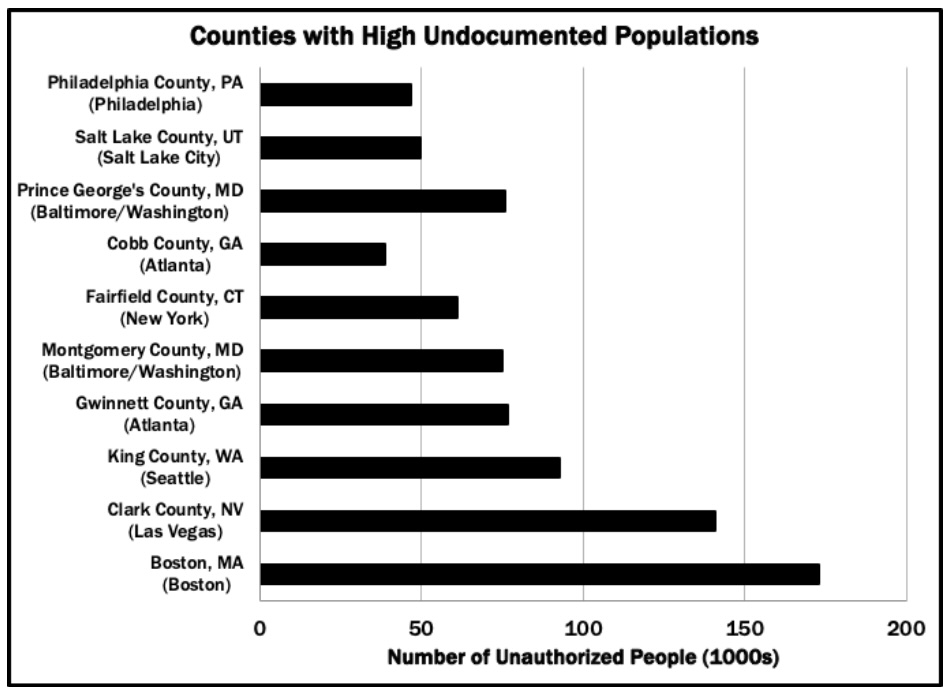

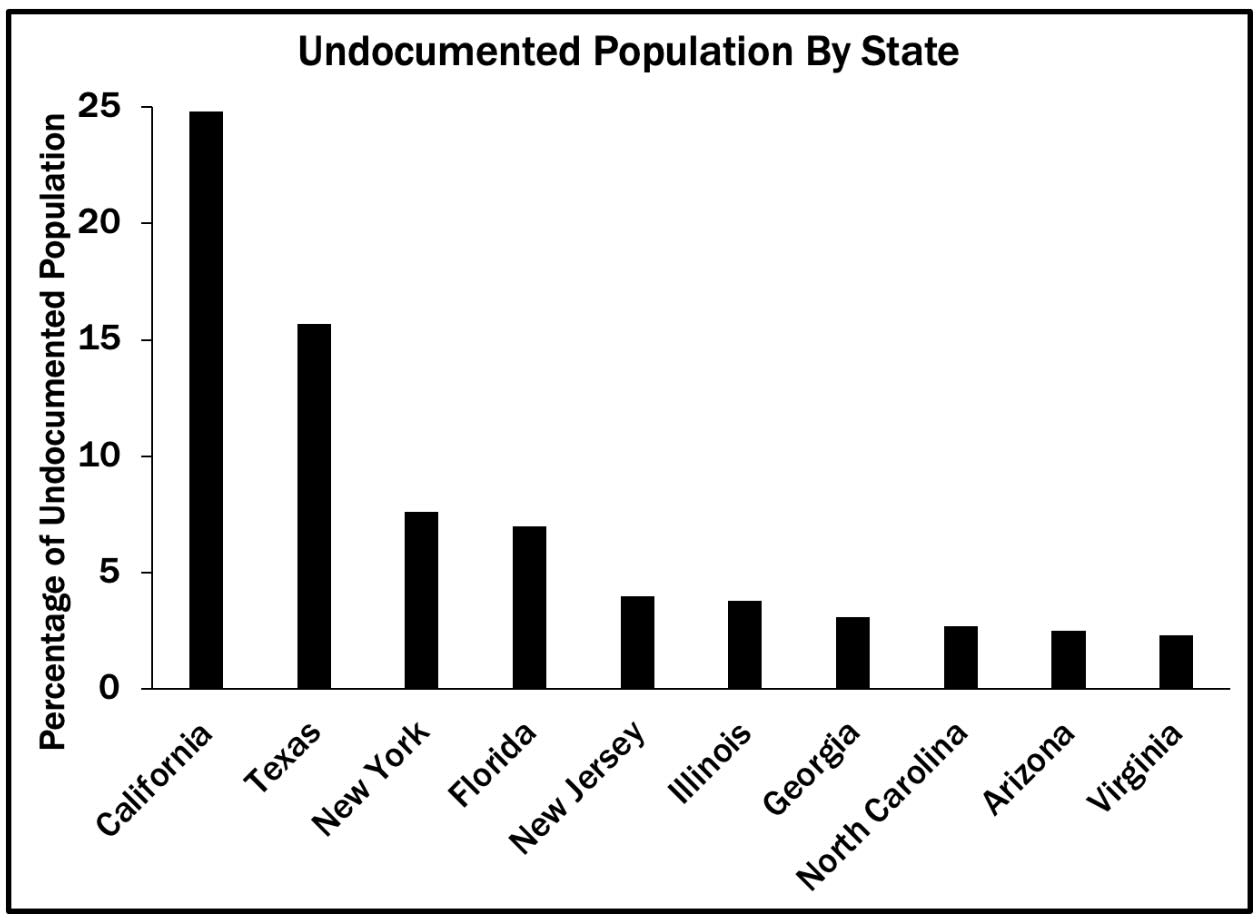

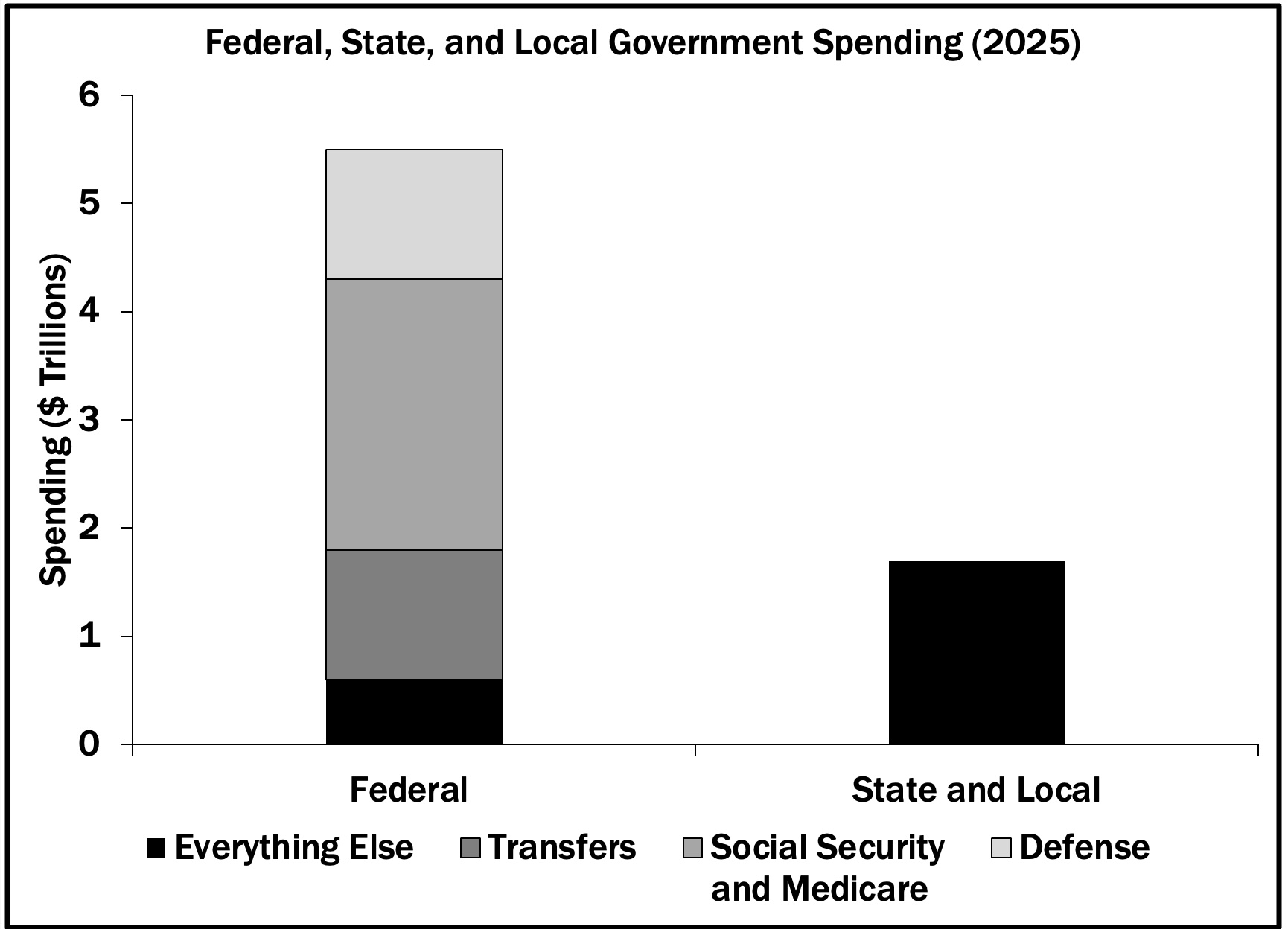

Gerry would be glad to see that state governments retain considerable policymaking power in areas such as education, public works, and zoning. Even today, most government employees work for state and local governments. Moreover, as the figure below shows for Fiscal Year 2025 (ending September 30, 2025), while the federal budget is considerably larger than state and local budgets, much of these funds are spent on defense, Social Security and Medicare, and transfers to state and local governments. With these areas excluded, state and local governments spend considerably more on the services most Americans use on a daily basis.

Gerry’s concerns would likely focus on the amount of money the federal government transfers to the states and the power these transfers confer. For example, about half of state spending on healthcare (primarily through the Medicaid health care program for the poor) is funded by the federal government. The federal government also provides a substantial share of funding for roads, mass transit, and other public works.

Federal assistance to states often comes with strings attached – constraints the federal government imposes on state policy as a condition of receiving the funds. This practice is sometimes labeled “coercive federalism,” reflecting the influence these transfers exert over policy. States can reject the federal mandates, but only if they are willing to forgo federal assistance and pay the difference themselves.

The Takeaway

Elbridge Gerry was a strong advocate of federalism during the writing and ratification of the Constitution.

Whether Gerry would object to the vast increase over the last two centuries in the size of the federal government is an open question.

He would surely object to the federal government’s practice of using transfers to sidestep the 10th Amendment to the Constitution, seeing it as a reversal of the compromises he and the other Antifederalists won during the debates over ratification of the Constitution.

.png)

.png)